Most people think about taxes in one simple way:

“How much income did I make?”

That matters, of course. But it is not the whole story.

A better question is:

“What kind of income did I create?”

That distinction can make a meaningful difference.

A dollar of salary, a dollar of capital gains, and a dollar borrowed against an asset may all help fund a lifestyle. But they are not treated the same way for tax purposes. That is why business owners, executives, and investors often spend so much time thinking about structure—not just income.

This is not about tricks or loopholes. It is about understanding the rules and planning wisely.

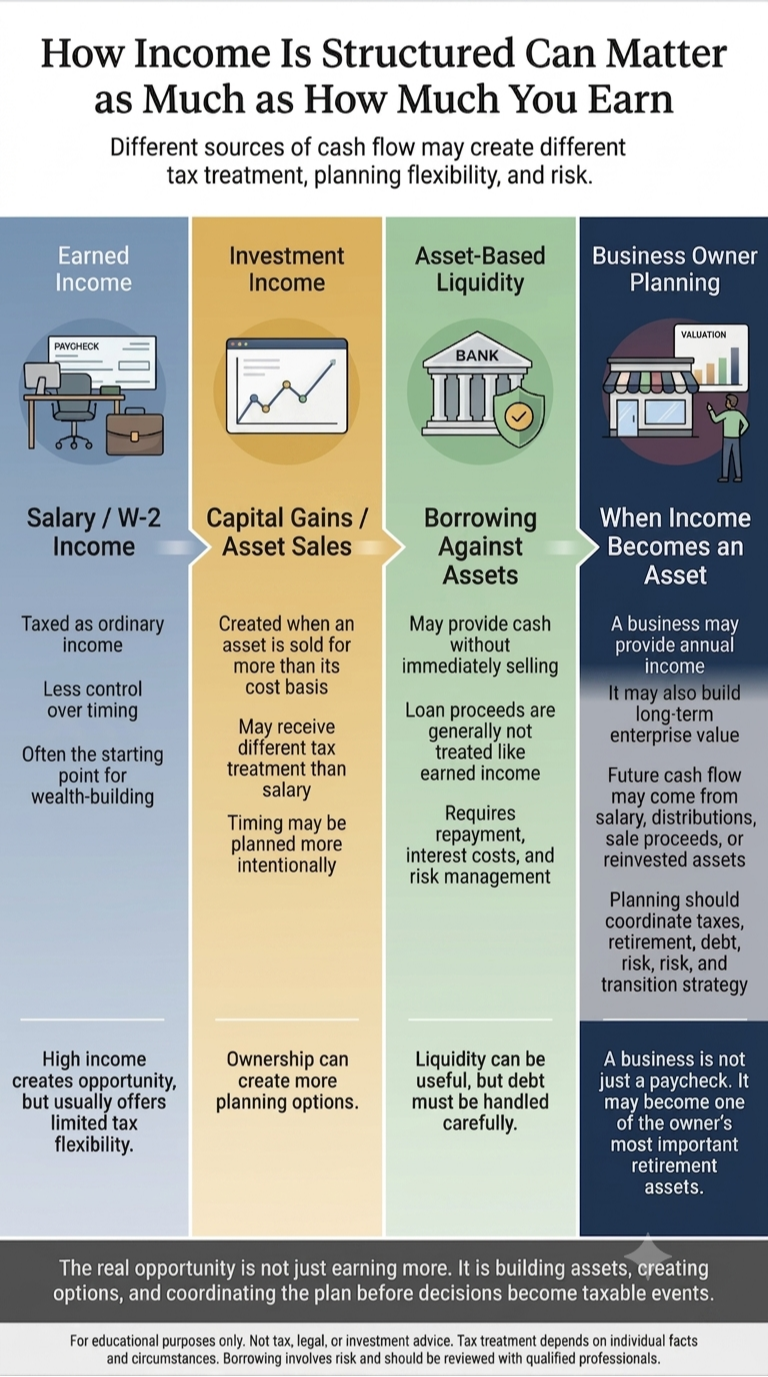

Check out this graphic, and then let's break it down simply:

1. Earned Income: High Income, Less Flexibility

Earned income is the money most people are most familiar with—salary, bonuses, wages, and business income tied directly to work.

This income is generally taxed as ordinary income. For high earners, that can mean a meaningful percentage goes to federal income taxes, state taxes where applicable, payroll taxes, and other related obligations.

There is nothing wrong with earned income. In fact, earned income is often the engine that creates opportunity.

But it usually offers limited flexibility.

You earn it.

It is reported.

It is taxed.

For many families, this is where wealth-building begins—but it is rarely where advanced planning ends.

2. Investment Income: Ownership Creates More Control

Investment income works differently.

When someone sells a capital asset—such as stock, real estate, or a business interest—the tax result is generally based on the difference between what was paid for the asset and what the asset is sold for. The IRS refers to this difference as a capital gain or capital loss. [irs.gov]

In many cases, long-term capital gains may be taxed at lower rates than ordinary income. [irs.gov]

That does not mean investment income is “tax-free.” It is not.

But ownership can create more planning flexibility:

- You may have some control over when an asset is sold.

- You may be able to plan around gains and losses.

- You may be able to coordinate the sale of an asset with charitable giving, retirement income planning, estate planning, or business transition planning.

This is one reason ownership matters.

A person who only earns income from labor has fewer planning levers. A person who builds assets may eventually have more choices.

3. Asset-Based Liquidity: Accessing Cash Without Selling

There is another layer that often gets discussed poorly online: borrowing against assets.

The basic concept is simple.

If someone owns a valuable asset—such as a portfolio, real estate, or a business interest—they may be able to borrow against that asset rather than sell it.

The borrowed money is not the same as income from a tax standpoint because it creates an obligation to repay. That is the key distinction. A loan is not a gift. It is not earnings. It is debt.

That can allow someone to access liquidity without immediately selling the asset and triggering a capital gain.

But this part deserves a big caution label.

Borrowing against assets is not magic. It introduces risk.

Loans have interest costs. Asset values can decline. Lenders can change terms. Cash flow has to support repayment. Used poorly, debt can turn a strong balance sheet into a fragile one very quickly.

So the lesson is not, “Borrow money and avoid taxes.”

The better lesson is:

Strong assets create options. Wise planning decides which options are worth using.

Real-World Example: The Business Owner

Imagine a business owner who has spent years building a profitable company.

For many years, most of the owner’s income came from the business itself. That income helped support the family, pay the bills, and fund retirement savings. But because it was active business income, much of it was taxed annually as it was earned.

Over time, though, the business became more than just a paycheck.

It became an asset.

That changes the planning conversation.

Instead of only asking, “How much income did the business produce this year?” the owner can begin asking better questions:

- What is the business worth?

- How much of my net worth is tied up in the company?

- Can the business support my lifestyle without over-relying on salary?

- Should I reinvest, take distributions, sell a portion, or eventually transition ownership?

- How do taxes, debt, retirement income, and estate planning fit together?

At that stage, income planning becomes much more than a tax return exercise.

The owner may have several possible sources of future cash flow:

- Salary or distributions from the business

Useful, but often taxable as income in the year received. - Proceeds from selling part or all of the business

Potentially taxed differently than ordinary income, depending on structure, basis, entity type, and other details. - Borrowing against business or investment assets

May create liquidity without an immediate sale, but also introduces debt, repayment obligations, and risk. - Investment income after an eventual transition

If the business is sold, the proceeds may need to be converted into a retirement income strategy.

This is where planning matters.

The goal is not simply to reduce taxes in one year. The goal is to coordinate the entire picture:

business value, personal income, taxes, retirement goals, debt, risk, and legacy.

A well-built business can create wealth.

A well-built plan helps turn that wealth into contentment, flexibility, and long-term fulfillment.

The Real Lesson: Wealth Is Built on Structure

The point of this illustration is not that one type of income is “good” and another is “bad.”

Salary can be good.

Business income can be good.

Investment gains can be good.

Borrowing can be useful in the right situation.

The key is understanding that each one behaves differently.

For clients building wealth, the goal is not simply to make more money. The goal is to build a financial structure that creates:

- reliable income,

- long-term growth,

- tax awareness,

- liquidity,

- flexibility,

- and resilience when life does not go according to plan.

That is where planning becomes valuable.

Not because planning eliminates taxes.

It does not.

Planning helps make sure decisions are coordinated—so income, investments, business value, retirement goals, risk management, and estate strategy are all working together instead of fighting each other.

Bottom Line

High income can create opportunity.

But high income by itself does not guarantee financial strength.

The families and business owners who tend to make the best long-term decisions are usually not just asking, “How much can I make?”

They are asking better questions:

- How is my income structured?

- Where is my wealth actually being built?

- How much control do I have over timing?

- What risks am I taking to create liquidity?

- How does this decision affect my long-term plan?

Those are the questions worth asking before the tax bill arrives—not after.

_______________________________________________________________________

Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS). OSJ: 6455 S. Yosemite Street, Ste 425, Greenwood Village CO, 80111, 303-7709020. Securities products and advisory services offered through PAS, member FINRA, SIPC. Financial Representative of The Guardian Life Insurance Company of America® (Guardian), New York, NY. PAS is a wholly owned subsidiary of Guardian. RISE Wealth Strategies is not an affiliate or subsidiary of PAS or Guardian. CA Insurance License Number - 4100103. Guardian, its subsidiaries, agents and employees do not provide tax, legal, or accounting advice. Consult your tax, legal, or accounting professional regarding your individual situation. The information provided is based on our general understanding of the subject matter discussed and is for informational purposes only. This material is intended for general use. By providing this content The Guardian Life Insurance Company of America and your financial representative are not undertaking to provide advice or make a recommendation for a specific individual or situation, or to otherwise act in a fiduciary capacity. 8987132.1 Exp. 6/28