You've probably heard people say "I'm in the market" or "I lost money when the market crashed." But what does that actually mean? What is the stock market, and how does it really work?

Let me break this down in plain English, because understanding these fundamentals changes everything about how you invest.

Stocks Are Ownership, Not Gambling Chips

When you buy a share of stock, you're not placing a bet. You're not buying a lottery ticket. You're buying actual ownership in a real company.

That share certificate (even though it's digital now) represents a fractional claim on everything that company owns and earns. Buy 100 shares of ABC Corporation? You own a tiny piece of ABC's factories, patents, cash reserves, and future profits. It's actual equity – hence why stocks are called "equities."

This matters because it fundamentally changes how you should think about market movements. When stock prices drop, you still own the same piece of the same company. The business didn't disappear. Only the price changed.

The Two Ways Investors Make Money

Capital Appreciation: The company grows and becomes more valuable. If ABC Corporation increases product sales, expands services revenue, or develops breakthrough products, the business becomes worth more. Your ownership stake rises accordingly. Buy a share at $100, sell it at $150 – that's a 50% capital gain.

Dividends: The company shares profits directly with owners. Mature, profitable companies often distribute cash to shareholders quarterly. Own 1,000 shares of a stock paying $2 annual dividends? You receive $2,000 per year regardless of whether the stock price goes up or down. These payments represent your share of actual business earnings.

Many successful investors focus heavily on dividend-paying stocks because dividends provide:

- Consistent cash flow during market volatility

- Evidence the company generates real profits (not just theoretical future growth)

- Compound growth when dividends are reinvested to buy more shares

The Two Ways Investors Lose Money

The business fails to perform. If a company loses market share, faces obsolescence, or executes poorly, the underlying business becomes less valuable. Your ownership stake declines with it. Blockbuster shareholders learned this the hard way when Netflix disrupted the industry.

You sell during a downturn. Here's where investors can destroy their wealth: they panic during market crashes and lock in losses by selling. The business might be fine, but fear drives them to sell at exactly the wrong time.

What Actually Moves Stock Prices

This is critical to understand: Stock prices don't move solely based on current company performance. They move based on what millions of investors collectively believe the company will do in the future.

That's why you see companies report record earnings but their stock drops – because investors expected even better results. Or why a money-losing startup trades at astronomical valuations – because investors believe future profits will justify today's price.

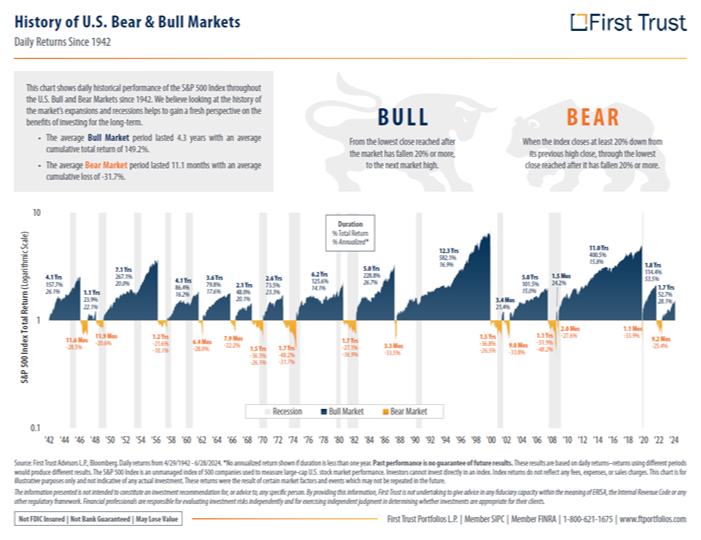

The Historical Pattern: Bulls and Bears

Since 1942, the stock market has moved through clear cycles of expansion and contraction.[1] Understanding this historical pattern provides crucial context:

Bull Markets (rising prices):

- Average duration: 4.3 years

- Average cumulative return: 149.2%

- Average annualized return: 16.9%

Bear Markets (declining prices):

- Average duration: 11.1 months

- Average cumulative loss: -31.7%

Let that sink in. Markets go up more than they go down. They go up for longer periods than they go down. And the gains during bull markets far exceed the losses during bear markets.

This is why legendary investor Brian Wesbury, Chief Economist at First Trust Advisors, has consistently emphasized the long-term upward trajectory of markets despite short-term volatility. The data supports patient, disciplined investing through market cycles.[2]

Why Bear Markets Feel Worse Than They Are

Even though bear markets have historically been shorter and shallower than bull markets, they feel devastating because:

Losses hurt more psychologically than gains feel good. Behavioral economics shows that losing $10,000 causes about twice the emotional pain as gaining $10,000 causes pleasure. Your brain is wired to overreact to losses.

Media amplifies fear. "Market crashes!" generates more clicks than "Market steadily climbs over decades." You're bombarded with panic-inducing headlines during downturns.

Recency bias clouds judgment. Whatever happened most recently feels like it will continue forever. During crashes, it seems like markets will never recover. During booms, it feels like growth is permanent.

But look at the data. The longest bear market since 1942 lasted just 1.7 years. The longest bull market? 12.3 years.[1]

The Investor Behavior That Determines Outcomes

Here's the uncomfortable truth: Most investors underperform the market significantly, not because they pick bad stocks, but because they react emotionally to volatility.

The successful behavior: Understand that stocks represent ownership in real businesses. Don’t move in an out of stocks based on emotions or feelings. Consider systematic contributions no matter what’s going on in the market (dollar cost averaging). Allow the principles of compound growth to work over decades.

The unsuccessful behavior: Panic during corrections and sell. Try to time the market by moving in and out. Stop contributing when prices feel "too high" or "too uncertain."

While past performance does not indicate future results, the S&P 500 has delivered roughly 10% average annual returns over the past century. Yet the average investor has earned barely half that – around 5% – because of poor timing decisions driven by emotion.[3]

What This Means for Your Investment Strategy

Understanding how the market actually works leads to several practical conclusions:

Own quality businesses, not just ticker symbols. If you wouldn't be comfortable owning a private business with similar fundamentals, why own the stock? Focus on companies with durable competitive advantages, strong balance sheets, and consistent earnings.

Expect volatility, don't fear it. Bear markets are normal, temporary, and historically have created the best buying opportunities. If you can't handle watching your account value drop 30% for 6-12 months, you're either too heavily invested in stocks or you don't understand what you own.

Time in the market beats timing the market. The data is overwhelming: staying invested through cycles has historically produced far better results than attempting to move in and out at "optimal" times. Nobody consistently times the market successfully.

Dividends provide ballast. Companies that pay consistent dividends tend to be more stable, more mature, and more focused on shareholder returns than pure growth stocks. Dividend payments also reduce your reliance on capital appreciation alone.

The Stock Market Serves a Purpose

At its core, the stock market exists to connect businesses that need capital with investors who have capital. Companies use stock offerings to raise money for expansion, research, acquisitions. Investors provide that capital in exchange for ownership stakes and the potential for returns.

This isn't abstract. When you buy stock in a company building renewable energy infrastructure, you're funding that development. When you own shares in a pharmaceutical company, you're financing drug research. Your capital helps enable business operations that create jobs, products, and economic growth.

The market facilitates this capital allocation efficiently (though not perfectly). It allows you to become a business owner with a few hundred dollars instead of needing millions to start your own company.

The Bottom Line

The stock market isn't magic or mystery. It's a mechanism for buying and selling ownership stakes in real businesses. Prices fluctuate based on collective expectations about future business performance.

Investors who understand this – who think like business owners rather than speculators – see more consistent results than those who treat stocks as gambling chips. They stay calm during volatility because they know the underlying businesses keep operating. They continue contributing during crashes because they recognize the opportunity. They collect dividends and allow compound growth to work over decades.

History shows that patient, disciplined investors who stay invested through complete market cycles capture the significant long-term gains that equities can help provide. The average bull market's 149% return more than compensates for the average bear market's -32% loss – but only if you remain invested through both.[1]

What questions do you have about how the stock market works? Understanding these fundamentals is the foundation for every investment decision you'll make.

_____________________________________________________________

References

[1] First Trust Advisors L.P., "History of U.S. Bear & Bull Markets - Daily Returns Since 1942," Bloomberg data through June 28, 2024, https://www.ftportfolios.com

[2] Brian Wesbury, Chief Economist, First Trust Advisors L.P., economic analysis and market commentary, https://www.ftportfolios.com

[3] DALBAR Quantitative Analysis of Investor Behavior, annual studies measuring investor returns vs. market returns

Raymond is a Financial Advisor and Executive VP of Operations at RISE Wealth Strategies, where purpose and wealth align. He helps individuals and families understand market fundamentals and build investment strategies grounded in business ownership principles rather than speculation.

The opinions expressed are those of the author and not necessarily those of Guardian or its subsidiaries. Past performance is not a guarantee of future results.

All investments and investment strategies contain risk and may lose value. Diversification does not guarantee profit or protect against market loss. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Investing in securities of smaller companies tends to be more volatile and less liquid than securities of larger companies. Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit and inflation risk. This material is intended for general use. By providing this content Park Avenue Securities LLC and your financial representative are not undertaking to provide investment advice or make a recommendation for a specific individual or situation, or to otherwise act in a fiduciary capacity. Indices are unmanaged and one cannot invest directly in an index.

Links to external sites are provided for your convenience in locating related information and services. Guardian, its subsidiaries, agents and employees expressly disclaim any responsibility for and do not maintain, control, recommend, or endorse third-party sites, organizations, products, or services and make no representation as to the completeness, suitability, or quality thereof.

Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS). OSJ: 6455 SOUTH YOSEMITE STREET, SUITE 425, GREENWOOD VILLAGE CO, 80111, 303-7709020. Securities products and advisory services offered through PAS, member FINRA, SIPC. Financial Representative of The Guardian Life Insurance Company of America® (Guardian), New York, NY. PAS is a wholly owned subsidiary of Guardian. RISE WEALTH STRATEGIES is not an affiliate or subsidiary of PAS or Guardian. CA Insurance License Number - 4100103. This material is intended for general use. By providing this content The Guardian Life Insurance Company of America, Park Avenue Securities LLC, affiliates and/or subsidiaries, and your financial representative are not undertaking to provide advice or make a recommendation for a specific individual or situation, or to otherwise act in a fiduciary capacity. Guardian, its subsidiaries, agents and employees do not provide tax, legal, or accounting advice. Consult your tax, legal, or accounting professional regarding your individual situation. Links to external sites are provided for your convenience in locating related information and services. 8748859.5 Exp. 3/28