Let me start with a confession: I spend a lot of time talking people out of their assumptions about taxes.

Just last week, I had a conversation with a couple in their mid-30s who'd been aggressively maxing out their 401(k)s for years—which is generally great financial behavior. But when I asked about their non-retirement savings, the wife said something I hear constantly: "We don't really use a regular investment account because we don't want to deal with all the taxes."

I get it. The conventional wisdom is clear: retirement accounts good, taxable accounts bad. Tax-deferred beats taxable every time. Max out the 401(k) before you even think about a regular brokerage account.

Except that's not actually true. And the misunderstanding costs people—both in flexibility and, ironically, in taxes they don't actually have to pay.

The Case for "Regular" Investment Accounts

Here's what I mean by a regular investment account: a standard brokerage account with no retirement designation. No age restrictions. No required minimum distributions. No early withdrawal penalties. No contribution limits. No rules about what you can or can't use the money for.

Just... an investment account.

These accounts have some genuinely compelling advantages:

- Flexibility: You can access your money anytime without penalty. Want to buy a house at 35? Start a business at 42? Help a kid with college at 50? The money's available without jumping through hoops or paying penalty fees.

- No required minimum distributions: Unlike IRAs and 401(k)s, nobody forces you to start taking money out at age 73. You control the timing.

- Tax diversification: Having money in different tax buckets—pre-tax retirement accounts, Roth accounts, and taxable accounts—gives you options for managing your tax bill in retirement.[1]

- Estate planning benefits: Investments in taxable accounts get a "step-up in basis" when you die, which can reduce or eliminate capital gains taxes for your heirs entirely. (Try getting that benefit from your IRA.)[2]

But here's the objection I always hear: "Yeah, but I'll get killed on taxes if I sell anything."

That's where we need to talk about how capital gains taxes actually work. Because many people—even in the financial services industry—fundamentally misunderstand the mechanics.

The Investment Gains Tax That Isn't What You Think

When you sell an investment in a taxable account for more than you paid, that profit is a capital gain. If you held the investment for more than a year, it's a long-term capital gain.[3]

(If you held it for a year or less, it's a short-term capital gain and gets taxed as ordinary income—which is genuinely worse. So we're focusing on long-term gains here, because that's what matters for buy-and-hold investors.)

Here's what most people think happens: "I have a $50,000 gain, so I'll owe capital gains tax on $50,000 at whatever my tax rate is."

That's not quite right. There are two critical things to understand:

First, long-term capital gains are taxed at special preferential rates: 0%, 15%, or 20%—not at your regular income tax rates of 10% through 37%.[4] This is a huge deal that people underestimate.

Second, the rate you pay depends on something almost nobody understands: how your capital gains stack on top of your ordinary income.

Let me explain what I mean by that, because this is where it gets interesting.

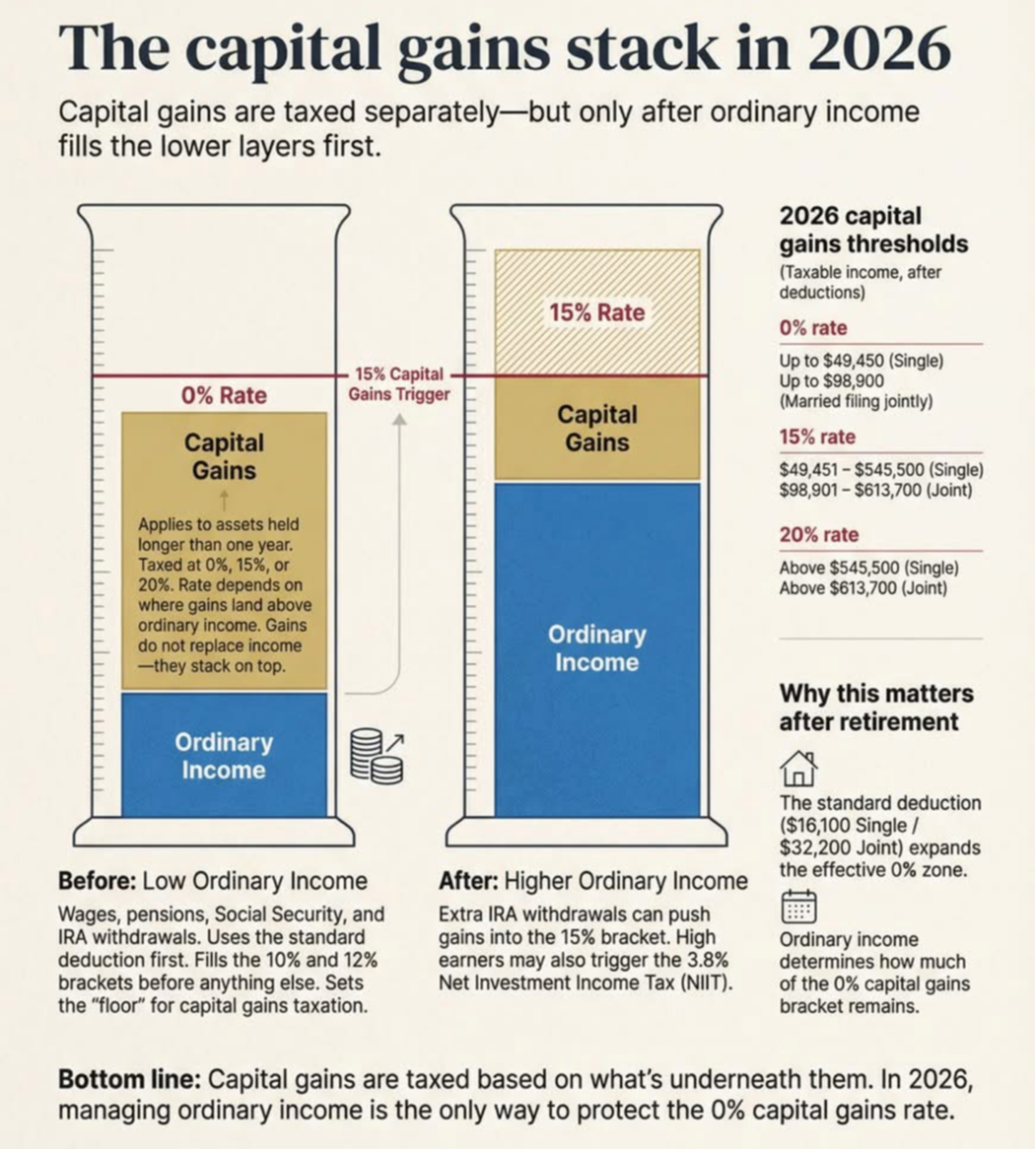

Capital Gains Stack On Top (And Why That Matters)

The U.S. tax system treats different types of income differently. Your wages, Social Security, IRA withdrawals, business income, interest—that's all "ordinary income" and gets taxed at regular rates.

Your long-term capital gains and qualified dividends get taxed at the preferential rates: 0%, 15%, or 20%.

But here's the key concept that changes everything: ordinary income always fills up the tax brackets first. Then your capital gains sit on top of that pile.[5]

Think of it like stacking blocks. Your ordinary income forms the foundation. Once that's in place, your capital gains stack on top. The capital gains tax rate you pay depends on where those gains land after your ordinary income is already accounted for.

This has three massive implications:

- Your capital gains cannot push your ordinary income into higher tax brackets. They're calculated separately.[6]

- Your ordinary income can push your capital gains into higher capital gains brackets. The more ordinary income you have, the less room you have for the 0% capital gains rate.[7]

- You might pay 0% federal tax on investment gains even while earning a decent income. This is the part almost nobody realizes.

Let me show you how this works with real numbers, because abstract tax concepts are about as useful as a screen door on a submarine.

How This Actually Works (Real Examples)

Example 1: The Early Retiree

Tom is 58 and took early retirement. He has $45,000 coming in from a pension and some part-time consulting work. He also needs to sell $25,000 worth of stock from his brokerage account to cover expenses.

For 2026, the standard deduction for single filers is $16,100.[8] So Tom's taxable ordinary income is $45,000 - $16,100 = $28,900.

That $28,900 fills up the first part of his tax brackets—all of it lands in the 10% and 12% brackets for ordinary income.

Now his $25,000 in long-term capital gains stacks on top of that $28,900. His total taxable income is $53,900.

Here's where it gets interesting: The 0% capital gains bracket for single filers extends to $49,450.[9] Tom's ordinary income only used up $28,900 of that space, which means he has $20,550 of room left in the 0% bracket.

So $20,550 of his gains are taxed at 0%. The remaining $4,450 is taxed at 15%.

Tom's federal capital gains tax: $668 (15% of $4,450).

On a $25,000 gain, that's an effective federal rate of 2.67%. Not exactly the tax disaster people imagine.

Example 2: The Married Couple Building Wealth

Mark and Lisa are both working and earn $95,000 combined. They've been investing in a regular brokerage account for years and have $40,000 in long-term gains they're considering taking this year.

After the married filing jointly standard deduction of $32,200, their taxable ordinary income is $62,800.[10]

The $40,000 in gains stacks on top, bringing their total taxable income to $102,800.

The 0% capital gains bracket for married couples extends to $98,900.[11] Since their ordinary income is $62,800, they have $36,100 of room left in the 0% bracket.

So $36,100 of their $40,000 gain is taxed at 0%. The remaining $3,900 is taxed at 15%.

Their federal capital gains tax: $585.

On a $40,000 gain. While both of them are working full-time with a combined six-figure income.

This is why understanding the stacking principle matters. Without knowing this, Mark and Lisa might avoid selling anything because they assume they'll face a big tax bill. In reality, they'd pay less than $600 in federal tax on a $40,000 gain.

The 2026 Numbers You Need to Know

For tax year 2026, here are the thresholds that matter:[12]

0% Long-Term Capital Gains Rate:

- Single filers: Up to $49,450 in taxable income

- Married filing jointly: Up to $98,900 in taxable income

15% Long-Term Capital Gains Rate:

- Single filers: $49,451 to $545,500

- Married filing jointly: $98,901 to $613,700

20% Long-Term Capital Gains Rate:

- Single filers: Above $545,500

- Married filing jointly: Above $613,700

Remember: these thresholds are based on taxable income—your income after the standard deduction or itemized deductions. This distinction matters enormously.

The standard deduction for 2026 is $16,100 (single) and $32,200 (married filing jointly).[13] This means a single person could have over $65,000 in combined income and deductions and still have room in the 0% capital gains bracket. A married couple? Over $131,000.

Why This Makes Regular Investment Accounts More Powerful

Understanding how capital gains taxation actually works changes the entire calculation about where to invest.

Scenario: You're 45 years old and maxing out your 401(k). You have an extra $1,000 per month to invest. Should you put it in a regular brokerage account or find another tax-advantaged option?

The conventional wisdom says: "Taxable accounts are for after you've maxed out all retirement accounts."

But consider what actually happens in a regular brokerage account:

- You invest after-tax dollars (no deduction now)

- The money grows

- When you sell, you pay capital gains tax on the profit—potentially at 0%, 15%, or 20%, depending on your income at that time

- You can access the money anytime without penalty

- If you hold until death, your heirs get a step-up in basis and pay no capital gains tax

Compare that to a traditional 401(k) or IRA:

- You invest pre-tax dollars (deduction now)

- The money grows tax-deferred

- When you withdraw, you pay ordinary income tax on everything—potentially 22%, 24%, or higher

- You can't access it before 59½ without penalty

- Your heirs pay ordinary income tax on inherited IRA withdrawals

Neither option is universally better. But the taxable account is nowhere near as bad as people think, and in many situations it's actually superior—especially when you understand that those capital gains might be taxed at 0%, 15%, or 20% instead of the 22%+ ordinary income rates you'd pay on IRA withdrawals.

The Retirement Planning Angle Nobody Talks About

Here's where this gets really strategic.

Most people spend their working years stuffing money into 401(k)s and IRAs. Then they retire and suddenly realize they have very little money in accounts they can access without creating taxable income.

Every dollar you pull from a traditional IRA or 401(k) is taxable ordinary income. That ordinary income fills up your tax brackets first and reduces the room you have for 0% capital gains treatment.[14]

But money in a regular brokerage account? You only pay tax on the gain, and potentially at preferential rates.

This is why sophisticated retirement planning often includes building up substantial taxable account balances—not as an afterthought, but as a core strategy. It gives you the flexibility to manage your tax bill by choosing which accounts to draw from in any given year.

Want to do a Roth conversion in a low-income year? Having taxable account money to live on while you convert IRA dollars makes that possible. Want to keep your ordinary income low to maximize the 0% capital gains bracket? You can't do that if all your money is in traditional retirement accounts.

What About the Downsides?

I'm not suggesting regular investment accounts are perfect or that you should abandon retirement accounts. There are legitimate trade-offs:

You don't get an upfront tax deduction. Money going into a 401(k) or traditional IRA reduces your taxes now. Money going into a brokerage account doesn't.

Dividends and interest are taxable annually. Even if you reinvest everything, you'll owe taxes on dividends and interest each year. (Though qualified dividends get the same preferential rates as long-term capital gains.)[15]

No creditor protection. Retirement accounts have legal protections in bankruptcy and lawsuits. Regular brokerage accounts generally don't.

But these downsides need to be weighed against the flexibility, access, and potentially lower tax rates on withdrawal. For many people—especially those already contributing enough to get their full employer match—building wealth in a taxable account makes tremendous sense.

From a Stewardship Perspective

Proverbs 21:5 says, "The plans of the diligent lead surely to abundance, but everyone who is hasty comes only to poverty."

Part of diligent planning is understanding how different financial tools actually work—not how we assume they work or how conventional wisdom says they work.

If you're avoiding regular investment accounts because you think the tax treatment is terrible, you're making decisions based on incomplete information. The tax treatment isn't terrible—it's often quite good, and in some cases better than retirement accounts.

Every dollar has a purpose in biblical stewardship, and part of our responsibility is understanding the tools available to us so we can make genuinely informed decisions.

The Bottom Line

A regular investment account—despite having no special retirement designation—can be one of the most effective ways to save and plan for your future.

The key is understanding how capital gains taxes actually work: they stack on top of ordinary income, they're taxed at preferential rates (0%, 15%, or 20%), and depending on your income situation, you might pay far less than you think.

This isn't about some exotic tax strategy or complicated loophole. This is just understanding the mechanics of how investment taxes are calculated so you can make informed decisions about where to build wealth.

Because at the end of the day, the best financial strategy isn't the one that sounds most impressive at cocktail parties. It's the one that actually works for your specific situation, gives you the flexibility you need, and doesn't cost you more in taxes than necessary.

What's your experience with taxable investment accounts? Have tax concerns kept you from using them, or have you found them more valuable than expected? Connect with me – I'd genuinely like to hear your perspective.

________________________________________________________________________________

** A 3.8% Net Investment Income Tax (NIIT) may apply to high-income earners. Some states may tax capital gains as ordinary income, adding to the federal rate.

References:

[1] Fidelity, "2025 and 2026 capital gains tax rates," October 20, 2025, https://www.fidelity.com/learning-center/smart-money/capital-gains-tax-rates

[2] Kiplinger, "Capital Gains Tax Rates 2025 and 2026: Updated Brackets, Rules and Comparison," January 14, 2026, https://www.kiplinger.com/taxes/capital-gains-tax/602224/capital-gains-tax-rates

[3] Internal Revenue Service, "Topic no. 409, Capital gains and losses," https://www.irs.gov/taxtopics/tc409

[4] Urban Institute, "How are capital gains taxed?" Tax Policy Center Briefing Book, https://taxpolicycenter.org/briefing-book/how-are-capital-gains-taxed

[5] FiPhysician, "Long-Term Capital Gains Stack on Top of Ordinary Income Tax," https://www.fiphysician.com/capital-gains-stack-on-top-of-ordinary-income/

[6] Kindness Financial Planning, "Capital Gains vs. Ordinary Income - The Differences + 3 Tax Planning Strategies," June 17, 2025, https://kindnessfp.com/capital-gains-vs-ordinary-income/

[7] Quarry Hill Advisors, "Can Capital Gains Push Me Into a Higher Tax Bracket?" July 1, 2025, https://quarryhilladvisors.com/blog/can-capital-gains-push-me-into-a-higher-tax-bracket

[8] Tax Foundation, "2026 Tax Brackets and Federal Income Tax Rates," https://taxfoundation.org/data/all/federal/2026-tax-brackets/

[9] CNBC, "How much you can make in 2026 and still pay 0% capital gains," October 14, 2025, https://www.cnbc.com/2025/10/14/capital-gains-taxes-2026.html

[10] Millan CPA, "2026 IRS Tax Brackets, Standard Deductions, Capital Gains +AMT," https://millancpa.com/insights/2026-irs-tax-brackets-standard-deductions-capital-gains-amt

[11] Kiplinger, "IRS Updates Capital Gains Tax Thresholds for 2026: Here's What's New," November 7, 2025, https://www.kiplinger.com/taxes/irs-updates-capital-gains-tax-thresholds

[12] CNBC, "IRS unveils higher capital gains tax brackets for 2026," October 10, 2025, https://www.cnbc.com/2025/10/09/capital-gains-tax-2026-federal.html

[13] Tax Foundation, "2026 Tax Brackets and Federal Income Tax Rates," https://taxfoundation.org/data/all/federal/2026-tax-brackets/

[14] Exchange Capital, "How Does Income Tax Work?" https://www.exchangecapital.com/wealthy-street-academy/educational-articles/how-does-income-tax-work

[15] VIP Wealth Advisors, "Capital Gains Tax Brackets 2025: How to Qualify for the 0%," August 28, 2025, https://vipwealthadvisors.com/insights/capital-gains-tax-brackets-2025-0-percent-rate

About the Author:

Raymond is a Financial Advisor and Executive VP of Operations at RISE Wealth Strategies, where purpose and wealth align. With a unique background combining ministry and financial services, he helps families navigate complex financial decisions through the lens of biblical stewardship principles while serving clients of all backgrounds. RISE specializes in values-based wealth management for families with $500K+ in assets across 30+ states.

Some scenarios and names mentioned herein are purely fictional and have been created solely for educational purposes. Any resemblance to existing situations, persons or fictional characters is coincidental. The information presented should not be used as the basis for any specific investment advice.

Registered Representative and Financial Advisor of Park Avenue Securities LLC (PAS). OSJ: 6455 South Yosemite Street, Ste 425, Greenwood Village, CO, 80111, 303-770-9020. Securities products and advisory services offered through PAS, member FINRA, SIPC. Financial Representative of The Guardian Life Insurance Company of America® (Guardian), New York, NY. PAS is a wholly owned subsidiary of Guardian. RISE WEALTH STRATEGIES is not an affiliate or subsidiary of PAS or Guardian. CA Insurance License Number - 4100103. This material is intended for general use. By providing this content The Guardian Life Insurance Company of America, Park Avenue Securities LLC, affiliates and/or subsidiaries, and your financial representative are not undertaking to provide advice or make a recommendation for a specific individual or situation, or to otherwise act in a fiduciary capacity. Guardian, its subsidiaries, agents and employees do not provide tax, legal, or accounting advice. Consult your tax, legal, or accounting professional regarding your individual situation. Links to external sites are provided for your convenience in locating related information and services. 8748859.10 Exp. 2/28